Why founders search for the best valuation tool for raising capital

If you are searching for the best valuation tool for raising capital, you are probably weeks from a pitch deck refresh or a term sheet conversation — and you know enterprise value alone misprices dilution. Investors ask pre-money equity value; lenders ask debt service coverage; your co-founder asks what the round does to walk-away proceeds. A single ARR multiple from a generic calculator cannot answer any of those precisely. The best valuation tool for raising capital runs Free Cash Flow to the Firm, Free Cash Flow to Equity, and EV/EBITDA in parallel, blends with capital-raiser persona weighting that emphasizes FCFE, and lets you scenario-test growth, hiring, and structure before you sign.

Exit Matters Chapter 5 focuses on cash flow to the owner — the lens capital raisers live in. Chapter 8 unpacks cost of capital — WACC, beta, credit spread — the drivers that move FCFF and FCFE when investors push on risk. Chapter 7 blends the three methods toward the decision in front of you. For fundraising, that means equity value clarity first, enterprise context second, market comps as sanity check third.

What capital raisers need that sellers and generic tools miss

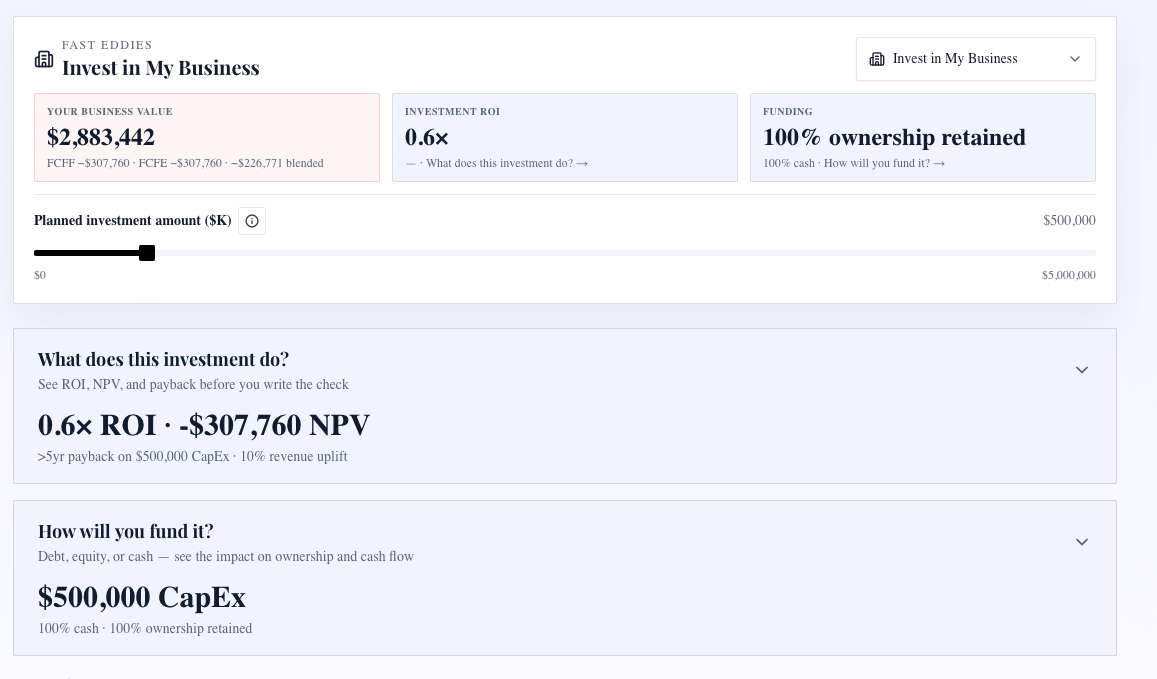

FCFE-forward blending. Dilution math requires knowing equity value after debt service and reinvestment — not just EV/EBITDA headline.

Cost of capital transparency. Investors stress-test WACC and growth assumptions. A tool that hides discount rates behind defaults fails diligence conversations.

Scenario engine for runway. "What if growth slows two points?" and "What if we delay the hire six months?" change FCFE and burn — model before the board meeting.

Industry band context. Market comps anchor expectations; premium drivers show which operational fixes expand pre-money before the round.

Living baseline. Fundraising spans months. Valuation must update as metrics improve — not freeze a number from last quarter's deck.

How XIT Matters supports capital raising

XIT Matters implements the Exit Matters capital-raiser workflow — free during public beta.

Six Persona Views include capital-raiser weighting that emphasizes FCFE while FCFF and EV/EBITDA provide enterprise and market context.

The Blended Valuation Engine combines all three methods into one equity-focused headline plus supporting tiles.

Cost of Capital Simulator exposes risk-free rate, beta, size premium, and credit spread — watch FCFF and FCFE respond when investors challenge risk assumptions.

Real-Time Slider Modeling adjusts growth rate, margin, customer concentration, and recurring revenue mix — every move recalculates instantly.

The AI Scenario Analyst accepts plain-English questions: "What if we raised prices 10% and churn stayed flat?" — mapping to coordinated lever moves across methods.

EV/EBITDA Market Comps anchor to SMB transaction multiples for your industry with premium and discount drivers visible.

QuickBooks and Xero compatible import or manual entry — ten minutes to first capital-raiser blend.

Approved trust claims: Built from Exit Matters, methodology used by PE firms, free during beta, ten minutes to your first valuation.

The pre-fundraise valuation playbook

Week 1: Baseline under capital-raiser persona. Connect financials. Document FCFE range, WACC assumptions, and industry band position. Share directionally with CPA — not full audit, just normalization sanity.

Weeks 2–6: Fix metrics investors underwrite. Customer concentration, net retention, rule-of-40, owner-independent sales motion — rank by FCFE delta per dollar. Execute top two fixes if runway allows.

Weeks 7–8: Scenario rehearsal. Model base, upside, and downside paths. Prepare answers for "what happens if growth slows?" before the partner meeting.

Pitch and term sheet: Anchor pre-money to capital-raiser blended FCFE range with three-method backup. Scenario outputs defend growth plan credibility.

Capital raising scenarios to model before term sheet

Pre-money from FCFE versus EV/EBITDA. Compare capital-raiser blend to seller-weighted blend — understand gap before investors anchor low on comps.

Dilution at various check sizes. Model equity issued at proposed valuations; confirm founder walk-away under each.

Growth versus profitability trade-off. Rule-of-40 and margin paths — show investors you modeled both sides.

Debt versus equity. Refinancing or venture debt impact on FCFE and covenants before choosing structure.

Customer concentration cleanup. Scenario reduced concentration — quantify WACC and multiple impact for investor narrative.

Common capital raising valuation mistakes

Quoting enterprise value when investors ask pre-money equity. FCFE clarity prevents headline confusion.

Using a single ARR multiple without cost of capital. Investors discount aggressive growth — show WACC sensitivity.

Static deck numbers while metrics improve weekly. Refresh blend before every investor update.

Skipping downside scenarios. Partners will stress-test; pre-run the floor.

Confusing preparation with binding appraisal. Use XIT for anchor; budget formal opinions when required.

Capital raising versus formal valuation — when each applies

Formal 409A, fairness opinions, and audited valuations govern specific legal and tax contexts. Investor pitch preparation and term sheet anchoring require speed and FCFE emphasis — the best valuation tool for raising capital delivers that in ten minutes free during beta. Escalate to formal work when counsel or tax requires signed opinions.

How to evaluate fundraising valuation tools in ten minutes

Confirm capital-raiser persona shifts blend toward FCFE. Verify WACC inputs are visible and adjustable. Run one growth or dilution scenario; confirm all three methods move. Check industry band with premium drivers. Ensure baseline updates without manual rebuild.

The bottom line for capital raisers

The best valuation tool for raising capital emphasizes FCFE within a three-method blend, exposes cost of capital, models dilution and growth scenarios, and stays live as metrics improve — free during beta in ten minutes. XIT Matters delivers that stack for founders who refuse to negotiate dilution from a single multiple guess. Know your equity range. Defend your plan. Raise from math, not hope.

SaaS and recurring-revenue founders — capital raiser specifics

If you raise on ARR narrative, investors still underwrite FCFE and cost of equity. Model net revenue retention, gross margin, rule-of-40, and customer concentration as live inputs — the same drivers that move SaaS EV/EBITDA bands. Capital-raiser persona weighting keeps equity value primary while market comps sanity-check pre-money against transaction data. The best valuation tool for raising capital must speak both languages: your growth story and the institutional math partners use to price risk.

Debt, venture debt, and FCFE — modeling before you sign

Venture debt and equipment lines change FCFE through covenants, amortization, and warrant coverage. Scenario refinancing versus equity raise before term sheet: compare FCFE walk-away, runway extension, and dilution. Founders who model debt first often discover equity need is smaller than gut feel suggested — or that covenants constrain growth assumptions investors will probe anyway. Cost of Capital Simulator ties credit spread to WACC so debt decisions flow through FCFF and FCFE together.

Board and investor update rhythm — keeping valuation live

Refresh capital-raiser blend before each board packet or investor update. Log metric changes — retention, margin, concentration — beside blended delta month over month. Investors notice when founders speak in FCFE ranges backed by three-method sensitivity instead of static deck slides from last quarter. The best valuation tool for raising capital earns its place in the fundraising stack when it updates as fast as your metrics, not when it produces one number you paste into slide fifteen and forget.

After the term sheet — still not binding, still useful

Signed term sheets trigger formal diligence — not the moment to stop modeling. Update scenarios with actual liquidation preference, pro rata rights, and option pool expansion. Confirm FCFE under closed structure before final signatures. XIT Matters remains preparation software, not legal or tax advice; pair live scenarios with counsel on final docs. Founders who keep modeling through close report fewer surprises on walk-away proceeds versus headline valuation.

Comparing capital-raiser tools — what to reject

Reject tools that quote enterprise value only when you need pre-money equity. Reject fixed 12 percent discount rates with no industry beta context. Reject static outputs that cannot scenario-test growth slowdown. Reject platforms that gate FCFE or WACC behind paid tiers during critical runway weeks. The best valuation tool for raising capital exposes equity math, cost of capital, and scenario sensitivity free during beta — the standard XIT Matters was built to meet for founders who cannot afford to negotiate blind.

Angel versus institutional rounds — persona weighting still applies

Angel rounds often negotiate from narrative and relationship; institutional rounds anchor to comps and FCFE math. Capital-raiser persona weighting prepares you for both — you can explain equity value intrinsically and relative to market band in the same conversation. Before angel meetings, stress FCFE and runway scenarios. Before partner meetings, stress WACC sensitivity and rule-of-40 or margin paths. The best valuation tool for raising capital lets you switch emphasis without rebuilding the model from scratch.

Cap table hygiene before you model dilution

Confirm outstanding options, warrants, and convertible notes before running pre-money scenarios. Missing cap table entries misstate FCFE and misprice dilution — investors discover errors fast. Export summary from your cap table tool, enter net share count and overhang assumptions, then model new money. Founders who clean cap table first report term sheet conversations that focus on growth plan credibility instead of arithmetic corrections in the data room.

When investors push back on your pre-money

Ask which lens they weight — FCFF, FCFE, or comps — and respond with sensitivity on that lens first. Show scenario downside you already modeled. Offer to update assumptions live if they challenge growth or margin — living tools beat static decks here. The best valuation tool for raising capital is negotiation software as much as math software when you can reproduce ranges and sensitivities in the meeting instead of promising follow-up spreadsheets.

Closing perspective for founders raising capital

Fundraising is a series of equity-value conversations disguised as growth story pitches. The best valuation tool for raising capital keeps FCFE, WACC, and dilution visible while you tell the story — free during beta, ten minutes to first range, live updates as metrics move. Founders who model before they pitch report sharper terms and fewer surprises at close because they negotiated from ranges they understood, not headlines they hoped would hold.

Bridge rounds and extension notes — scenario before you sign

Bridge financing and extension notes compress timeline pressure but often embed warrants, liquidation preferences, or punitive ratchets that shift FCFE materially. Model each structure under capital-raiser persona before signing — compare walk-away under base revenue path versus downside path. The best valuation tool for raising capital helps you see whether bridge economics cost more in dilution than waiting for a cleaner institutional round, even when runway feels tight today.

SAFE notes and convertible instruments — model conversion dilution

SAFEs and convertible notes stack into cap table overhang that surprises founders at priced rounds. Enter outstanding convertible instruments before modeling pre-money — conversion at cap or discount changes FCFE and effective dilution materially. Scenario priced round with and without full conversion so term sheet math matches reality investors already see in your data room. Founders who model conversion stacks before partner meetings avoid the awkward pause when legal reveals dilution nobody put in the deck.