What Is My SaaS Business Worth in 2026? The Honest Range, Not a Single Guess

If you are asking what is my SaaS business worth in 2026, the market has changed since the easy-money years. After the sharp re-pricing in 2022 and 2023, buyers today reward predictable recurring revenue, strong net retention, balanced growth and profitability, and businesses that can run without the founder doing every deal. A single ARR multiple pulled from a headline or a generic calculator is a starting point, not an answer you can defend in diligence or negotiation. The reliable path uses the same three institutional methods professional valuators apply — Free Cash Flow to the Firm, Free Cash Flow to Equity, and EV/EBITDA — then blends them into a range that respects your specific unit economics, growth trajectory, and risk profile.

Exit Matters Chapter 6 explains why buyers pay premiums for certain SaaS characteristics: recurring revenue reduces perceived risk and lifts the multiple because future cash flows are more visible and stable. Chapter 4 shows how to turn those cash flows into a present value through discounted cash flow. Chapter 3 reminds us that 80 percent directional accuracy you can act on today beats perfect precision delivered months from now. The result for most founder-run SaaS businesses in the $1M to $25M ARR band is a defensible range, not a single number you argue over.

The 2026 SaaS Multiple Band: 3.0× to 9.0× ARR

Current market data for SaaS businesses in the typical small-to-lower-middle-market range shows a wide but rational band. At the low end, 3.0× ARR applies to companies growing under 20 percent year-over-year, with net revenue retention at or below 95 percent, heavy founder dependence in sales, and top-customer concentration above 25 percent. These businesses look more like high-churn transaction businesses than durable subscription assets, so buyers apply heavy discounts.

The median sits around 5.5× ARR for companies delivering 25 to 35 percent growth, net retention between 100 and 110 percent, repeatable sales motions that do not require the founder on every call, and a rule-of-40 score in the low-to-mid 30s. This is the zone where most well-run vertical or horizontal SaaS businesses land when they have clean financials and some proof of defensibility.

The high end, 9.0× ARR and occasionally higher, is reserved for companies growing 35 percent or more, posting net retention above 110 percent, rule-of-40 above 40, low customer concentration, documented playbooks that let the business run without the founder, and often a vertical or regulatory moat that makes switching costly. Vertical SaaS serving regulated industries such as healthcare, financial services, or public sector frequently trades at the upper end of the band because the switching costs and compliance burden create natural retention.

These bands are not arbitrary. They reflect the Four Forces that Chapter 6 identifies as driving buyer multiples: risk reduction (recurring revenue and retention), growth visibility, capital efficiency, and owner independence. Improve any one and the multiple can expand; weaken any one and it compresses, sometimes by a full turn or more.

Why a Single ARR Multiple Is Not Enough — Run the Three Institutional Lenses

A revenue multiple feels simple but collapses the moment a buyer asks how you arrived at it or what happens to value if churn ticks up two points. Three independent methods give you a range you can explain and defend.

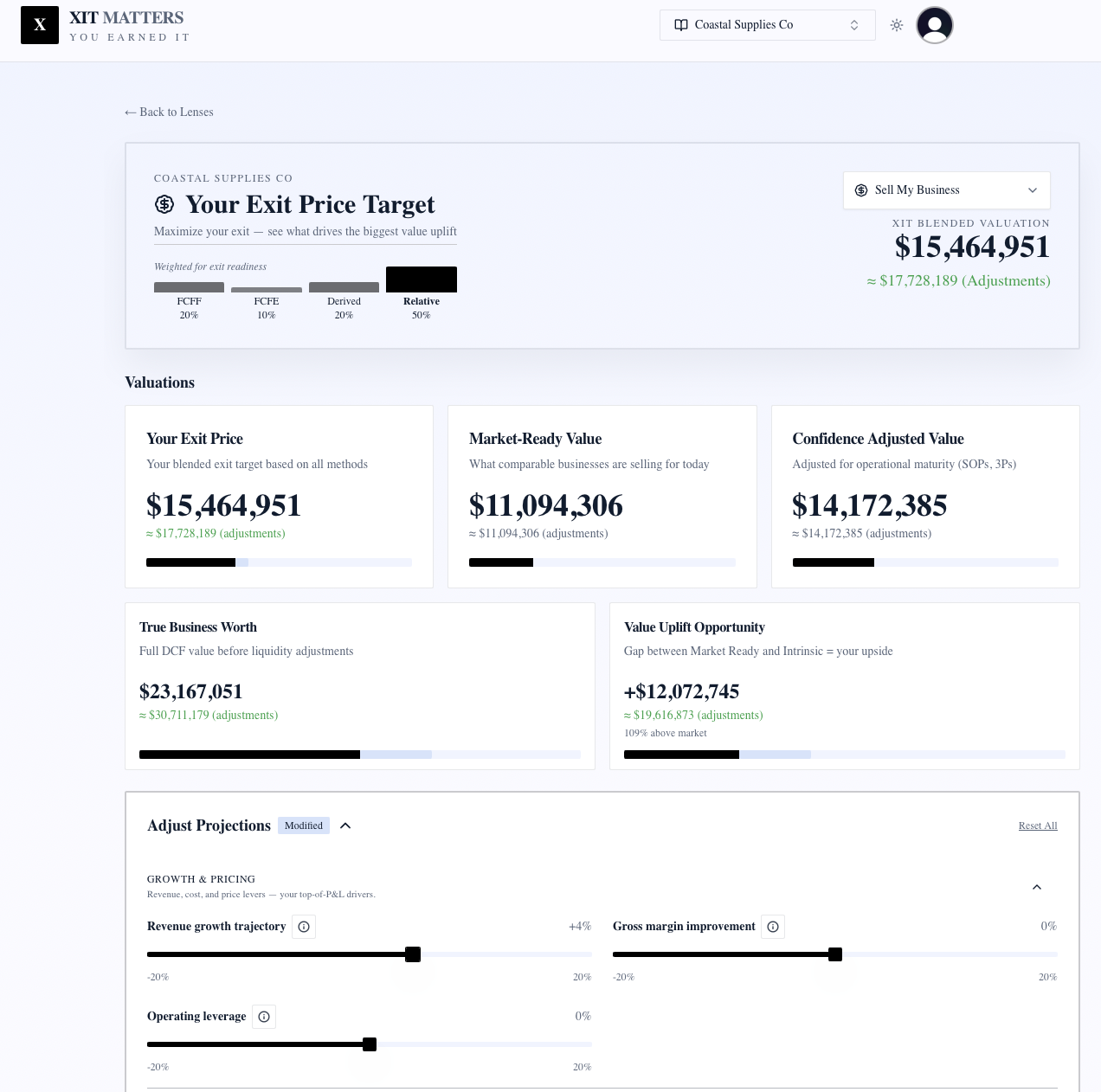

Free Cash Flow to the Firm (FCFF), or Lens 1 in the framework, projects the unlevered cash the operations will generate over the next five years, adds a terminal value assuming modest perpetual growth, discounts everything back at your weighted average cost of capital, and applies an illiquidity discount because private SaaS businesses are harder to sell than public stocks. For SaaS the WACC is often lower than for asset-heavy businesses because subscription cash flows are relatively predictable once retention is stable. Where this intrinsic value sits above the market multiple answer, you have a reinvestment story worth telling; where it sits below, you may have a strategic-fit argument that only certain buyers will pay for.

Free Cash Flow to Equity (FCFE), or Lens 2, applies the same machinery but after actual debt service and net borrowing. Most early-stage SaaS balance sheets are light on traditional debt, yet venture debt, convertible notes, or future dilution still affect what equity holders ultimately receive. This lens keeps the boundary clear between enterprise value and the slice that belongs to founders and investors after obligations.

EV/EBITDA, or Lens 3, anchors directly to what comparable transactions are paying today. Below roughly $10M ARR most SaaS businesses still trade primarily on revenue because EBITDA is negative or near zero while the company reinvests in growth. Above that scale with positive and growing EBITDA, the EV/EBITDA multiple becomes the cleanest comparison to financial-buyer comps. The multiple itself is adjusted for the same factors that drive the ARR band: retention, concentration, founder dependence, and rule-of-40. Chapter 6 shows how to decompose the multiple into its drivers so you can see exactly which of your metrics is moving the needle.

The Blended View combines the three lenses with weights that shift depending on whether you are running the business day-to-day (more cash-flow lenses) or preparing to raise capital or exit (more weight on the market lens). For a founder persona the default blend often lands between the pure intrinsic and pure market answers, giving you one number you can actually use in conversation.

What Actually Moves Your SaaS Valuation Up or Down

Growth rate remains the single largest lever. Each five-point improvement in year-over-year ARR growth can push the multiple toward the high end of the band, especially when paired with strong retention. The reverse is equally true: sub-20 percent growth caps most businesses at the low-to-middle part of the range no matter how good the rest of the metrics look.

Net revenue retention (or its inverse, churn) is the next biggest driver after growth. Net retention above 110 percent earns a premium because the existing customer base expands on its own; the buyer does not have to replace every lost dollar with new sales. Losing even 3 percent of revenue per month compounds into a material discount on the multiple because every forward projection starts from a smaller base. Chapter 6 highlights recurring revenue as one of the strongest risk-reduction signals buyers reward with higher multiples.

Rule-of-40 — simply year-over-year growth percent plus EBITDA margin percent — has become table stakes. Above 40 the market still tolerates heavy reinvestment; between 30 and 40 you are at median; below 30 the multiple compresses quickly because buyers see unsustainable cash burn or insufficient growth to justify the valuation. Post-2022 buyers are stricter on this metric than they were in 2021.

Top-customer concentration above 25 percent is a clear discount driver; above 40 percent it can become a deal killer for institutional capital because the loss of one client would crater the numbers. Owner or founder dependence is equally penalised. When the founder is still closing more than half of new business or is the only person who truly understands the product architecture, buyers apply a discount for key-person risk and for the work required to professionalise the go-to-market motion.

Recurring versus services mix matters because pure subscription revenue above 90 percent of total revenue earns the cleanest multiple. Anything above 30 percent services revenue, even if profitable, signals a business that may still be selling projects rather than scalable software. Gross margin below 70 percent compresses value; above 80 percent it supports the high end of the band because more of each incremental dollar drops to the bottom line.

These are not theoretical. Exit Matters Chapter 6 walks through how each of these factors maps to one of the Four Forces that ultimately determine the multiple a buyer will pay. Fix the underlying driver and the multiple follows.

Strategic Buyers Versus Financial Buyers — Your Range Is Usually the Floor

Financial buyers — private equity, growth equity, and other institutional capital — are anchored to rule-of-40, cash-on-cash returns, and the ability to improve the business over a five-to-seven-year hold. They will rarely pay above the top of the comp range unless the numbers are exceptional.

Strategic buyers — other SaaS companies acquiring for product fit, channel access, customer base, or talent — can and do pay above the financial-buyer band when clear synergies exist. The uplift can be 1× to 3× ARR or more depending on how much the acquirer can accelerate growth or cut costs by folding your product into theirs. In those conversations the XIT Matters range becomes your floor, not your ceiling. You walk in knowing what a financial buyer would pay and can negotiate upward from there with data rather than hope.

Chapter 6 notes that buyers ultimately pay for reduced risk and visible growth. A strategic acquirer sees additional risk reduction through integration; a financial buyer does not. The three-method range gives you the vocabulary to have both conversations without guessing.

A Worked Example: $3M ARR Vertical SaaS in Healthcare

Consider a vertical SaaS business serving healthcare credentialing, $3M ARR, 30 percent year-over-year growth, 108 percent net retention, 15 percent EBITDA margin, top customer representing 22 percent of revenue, and the founder still personally closing roughly 40 percent of net new bookings.

A generic calculator might simply apply 4× ARR and spit out $12M. That number is not wrong; it is just incomplete.

Running the three methods produces a more nuanced picture. The FCFF lens, using a five-year projection that fades growth toward a long-term 3 percent terminal rate and a WACC in the high single digits (reflecting relatively predictable subscription cash flows), lands in the $14M to $16M range. The FCFE lens is similar given a clean balance sheet with modest or no venture debt. The EV/EBITDA lens at the median 5.5× multiple on $2.5M of EBITDA implies roughly $13.75M; pushing toward the premium end of the SaaS band would suggest higher, but founder dependence and concentration cap the realistic outcome.

The Blended View for a founder or capital-raiser persona typically converges around $13.5M to $15M. A buyer can reasonably argue that founder dependency and concentration justify 4× to 4.5× ($12M to $13.5M). The seller can point to vertical regulatory moat, strong retention, and growth to support 5.5× to 6.5× ($16.5M to $19.5M). The math gives both sides a shared language and a clear set of levers to discuss. That is the difference between a single multiple and a defensible range.

How to Increase Your SaaS Business Value Before Exit

The highest-leverage moves are the same ones that appear in the XIT Matters scenario tools and that Chapter 6 identifies as moving the Four Forces.

Lift net revenue retention above 110 percent by building expansion revenue, better onboarding, and customer success motions that turn one-time buyers into growing accounts. Reduce top-customer concentration below 20 percent by deliberately diversifying the base and raising prices or limiting exposure on the largest clients. Document repeatable sales and onboarding playbooks so the business is no longer founder-led; this directly attacks owner-dependence risk and expands the multiple even before EBITDA moves. Finally, push the rule-of-40 score higher through some combination of growth and margin improvement while keeping cash conversion positive. Each of these moves expands the multiple before it necessarily changes trailing EBITDA, which is exactly why early action compounds into a materially higher exit.

The Tool That Turns “What Is My SaaS Business Worth” Into a Live Management Habit

XIT Matters runs the full three-method stack automatically once you connect QuickBooks or Xero (the two systems most SaaS founders already use) or enter the last twelve months of P&L and balance sheet manually. The SaaS-specific inputs — ARR growth rate, net retention, gross margin, top-customer concentration, founder-dependency percentage, and recurring-versus-services mix — appear as live sliders. Move any one and every lens plus the Blended View recalculates instantly.

The AI Scenario Analyst turns plain-English questions into precise outputs. Ask what happens if you close one more $250K ACV deal this quarter, raise prices 8 percent on the existing base, or lose a key customer, and it returns the dollar impact on FCFF, FCFE, EV/EBITDA, and the final blended number. All of it is grounded in your actual financials and the same methodology the book teaches, not generic rules of thumb.

For a founder this turns valuation from a once-a-year or pre-raise event into a weekly or monthly habit. You see which operational improvements actually move the number that matters and which ones are just busywork. The 80/20 Rule from Chapter 3 applies here: you do not need audit-grade precision every month. You need directional accuracy you can act on before the next board meeting or buyer conversation.

The 80/20 Truth: Start With a Good-Enough Range and Improve It

Most SaaS founders do not need a $50,000 formal appraisal to know where they stand or to prepare for a raise or exit. They need a defensible range they can explain and a clear set of levers to close the gap between where they are and where they could be. The three-method blended approach delivers exactly that in minutes rather than weeks.

Connect your financials, move the levers that match your real business story, and watch the range tighten or expand. The gap between your current Blended View and the high end of what the market would pay for a better version of your SaaS is the map for the next twelve months of work. That is how you multiply what your SaaS business is worth in 2026 — not by guessing a multiple, but by understanding and improving the drivers behind it.

Grounded in the four-lens framework, FCFF/FCFE/EV/EBITDA methodology, recurring-revenue and owner-dependence insights from Exit Matters Chapters 3, 4, and 6, and the author’s experience exiting a SaaS EdTech business. All case examples are composites drawn from real founder engagements to protect confidentiality while illustrating the decision framework.