Why every small business owner needs a valuation tool — not just sellers

If you typed "best tool to value my small business" into a search bar, you probably are not browsing for curiosity. Something concrete is driving the question — a partner conversation, a bank meeting, a potential acquisition, or the quiet realization that you have been running hard for years without knowing what you have built. Whatever the trigger, the wrong tool gives you a single revenue multiple that ignores half of what drives value. The right tool gives you a defensible range in one sitting and keeps it current as your business evolves.

Most small business owners track profit and cash because those numbers arrive every month. Valuation — what the entire operation is worth to a buyer, lender, or to you as the wealth holder — stays invisible until a crisis forces the question. That gap costs money. Owners who know their blended number make better decisions about pricing, hiring, capital expenditure, and timing. Owners who fly blind accept lowball offers, overpay for growth, and discover too late that their largest asset was underpriced by a full turn on the multiple.

Exit Matters Chapter 3 frames this as the 80/20 principle: capture most of the methodological insight in a fraction of the time and cost of a formal appraisal. Chapter 7 introduces the Blended View — three institutional methods weighted for your specific decision. Chapter 8 explains why your cost of capital is not a generic 12% guess but a calculation tied to your industry, capital structure, and risk profile. The best tool to value my small business implements all three chapters as software, not theory.

What "value" actually means for a small business

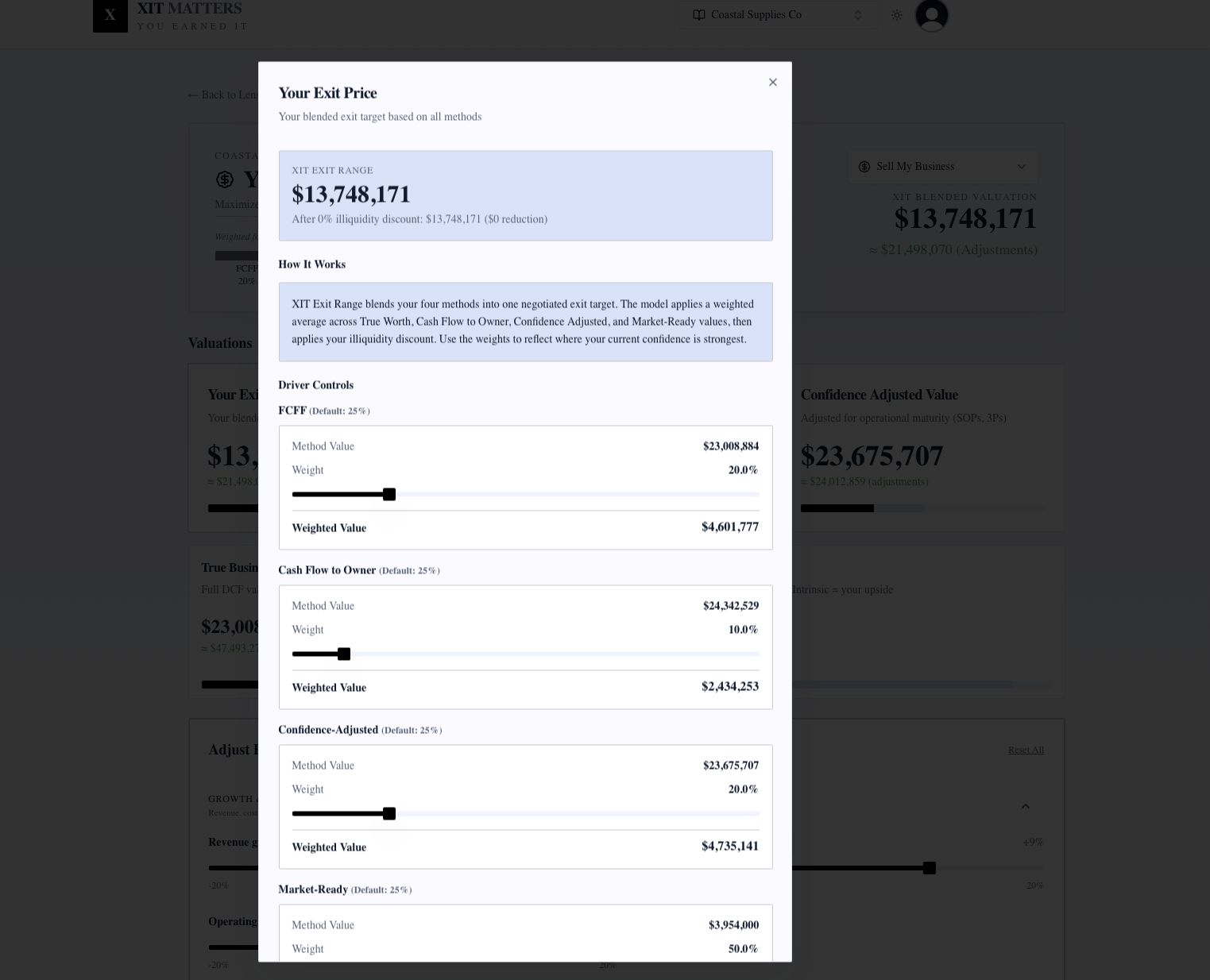

Value is not one number. It is a range produced by triangulating three independent methods that professional valuators have used for decades.

Enterprise value — what the whole business is worth

Free Cash Flow to the Firm (FCFF) projects the cash your operations generate for all capital providers — lenders and owners alike — discounts every dollar back to today using your weighted average cost of capital, adds a terminal value, and applies an illiquidity discount because private businesses cannot be sold on a stock exchange. The output is enterprise value: the worth of the machine before financing decisions.

Equity value — what your stake is worth

Free Cash Flow to Equity (FCFE) runs the same machinery after debt service and net borrowing. The output is what your shares are worth — the number that matters when you are modeling a partner buyout, evaluating a growth loan, or deciding what you could take home in an exit. Confusing enterprise value with equity value is one of the most expensive mistakes small business owners make.

Market value — what buyers actually pay

EV/EBITDA applies a transaction multiple to your normalized EBITDA based on what comparable small businesses have sold for in your industry. Multiples are the language brokers, SBA lenders, and acquirers speak. The risk is treating a multiple as a fact instead of a band — the best tool shows low, median, and premium for your sector and maps each to the qualitative drivers you control.

The Blended View combines all three with weights that shift based on your persona — active owner, seller, buyer, capital raiser. One business, different lenses, one actionable headline number.

How the best tool to value my small business beats spreadsheets and calculators

Three methods, not one. Revenue-multiple calculators give a single guess. Appraisals give three methods in a static PDF six weeks later. A living tool gives all three now and recalculates when anything changes.

Industry-calibrated multiples. Generic tools apply one multiple to every business. Serious tools load curated SMB transaction bands by sector — SaaS, e-commerce, professional services, restaurants, manufacturing — with premium and discount drivers displayed alongside the slider.

Cost of capital that respects your business. Many calculators use a fixed discount rate. Your real WACC depends on industry beta relevered to your debt-to-equity, effective tax rate, and credit spread. Moving those four levers and watching FCFF respond teaches you which capital-structure decisions actually shift value.

Real-time scenario modeling. "What if I raise prices 8%?" "What if I hire two reps at $70K each?" "What if I pay down $200K of debt?" The AI Scenario Analyst translates plain-English questions into exact input changes and shows dollar impact across every method.

Persona-aware blending. A seller weights EV/EBITDA higher because that is what a buyer will anchor to. An active owner weights FCFF because that reflects intrinsic worth. The tool encodes those weightings so the headline answer matches the decision in front of you.

Living, not static. Your business changes weekly. A valuation from January is stale by April. Connected accounting data means your number updates without manual rework.

How XIT Matters works as the best tool to value my small business

XIT Matters was built from the Exit Matters methodology for owners who need institutional-grade valuation without institutional-grade cost or wait time.

Onboarding takes about ten minutes via QuickBooks or Xero connection, or fifteen with manual entry. Select your industry to load the appropriate EV/EBITDA band. The owner persona activates by default, weighting the Blended View toward operational cash flow while keeping market comps visible.

Six approved features map directly to the valuation workflow:

- Blended Valuation Engine — FCFF, FCFE, and EV/EBITDA in one headline number with supporting tiles for each lens.

- AI Scenario Analyst — plain-English what-ifs translated to precise lever moves with dollar impact explanations.

- Six Persona Views — see the same business as a seller, buyer, investor, or capital raiser would.

- Cost of Capital Simulator — four sliders (credit spread, beta, debt paydown, tax rate) with industry benchmarks.

- Real-Time Slider Modeling — drag growth, pricing, working capital, or hiring assumptions and watch every method recalculate.

- EV/EBITDA Market Comps — trailing and forward EBITDA multiplied by curated SMB transaction multiples.

Trust claims are limited to what the product actually delivers: built from Exit Matters, methodology used by PE firms, QuickBooks and Xero compatible, free during beta, ten minutes to your first valuation.

Practical use cases beyond selling

Partner buyouts. FCFE shows what each partner's stake is worth today — essential when one partner wants out and emotions run high.

Growth financing. Walk into a bank with a three-method range instead of a guess. Lenders respect owners who understand their own capital structure.

Insurance and estate planning. Your business is likely your largest asset. A living valuation feeds estate planning conversations with real numbers instead of decades-old broker estimates.

Strategic decisions. Should you buy the competitor, open the second location, or invest in automation? Model each scenario and compare the blended valuation delta to the investment cost.

Annual wealth tracking. Treat business value like a portfolio holding — track it quarterly alongside other assets to understand total net worth trajectory.

Normalizing your numbers before you trust the answer

Garbage in, garbage out applies to every valuation method. Before running the three lenses, normalize earnings:

Replace owner compensation above market rate with a market salary for whoever would do the job post-acquisition. Add back personal expenses run through the business. Remove one-time items — legal settlements, disaster costs, pandemic-era grants. Adjust for non-arm's-length rent if you own the building. Smooth seasonal spikes if one quarter distorts the year.

XIT Matters flags low-confidence inputs and guides normalization without requiring CPA involvement for the directional answer. When you need binding precision for litigation or IRS purposes, bring in a professional — but you will walk in already knowing the range.

Common mistakes when valuing a small business

Using last year's revenue times three. Revenue multiples ignore profitability, capital structure, and industry-specific comp bands.

Waiting for perfect books. Imperfect data with flagged assumptions beats no valuation at all. Start now and refine as accounting cleans up.

Ignoring illiquidity. Private business equity is not tradable like public stock. A defensible tool applies an illiquidity discount and lets you stress-test the assumption.

Valuing once and forgetting. Business value compounds or erodes with every decision. A living tool makes that visible; a one-time report does not.

Choosing the cheapest calculator. Free revenue-multiplier widgets cost nothing upfront and everything at the negotiation table when you accept a number you cannot defend.

Building a quarterly valuation habit as a small business owner

The best tool to value my small business pays off when you use it on a rhythm, not once. After each month-end close, skim the blended headline and note what moved — a new hire, a price increase, a debt paydown, a lost contract. Over four quarters you build an intuition for which levers actually shift FCFF versus which ones only change revenue on the P&L.

Once per quarter, pick one strategic question and run it through the AI Scenario Analyst: Should we open the second location? Can we afford the automation line? What happens if we raise prices 6% and lose two accounts? The dollar answer across all three methods beats gut feel when you are allocating scarce capital.

Share the range with your CPA or bookkeeper annually so normalization stays aligned with how a buyer would rebuild EBITDA. When you eventually sell, partner out, or borrow, you will not be starting from zero — you will have years of living data showing how value compounded with the decisions you made.

The owners who get the most from the best tool to value my small business are the ones who treat the blended headline like they treat revenue — a KPI reviewed on schedule, questioned when it moves, and tied to explicit decisions. That habit turns valuation from an abstract finance exercise into the scoreboard your business deserves.

When you present a range backed by FCFF, FCFE, and EV/EBITDA, lenders and partners engage differently. They ask better questions because you opened with methodology instead of hope. That shift alone justifies ten minutes of setup — and it is why owners searching for the best tool to value my small business increasingly choose living three-method platforms over static calculators. Start today with imperfect books; refine tomorrow with cleaner data. Your future self — at the bank, the partner meeting, or the closing table — will thank you for the habit.

The bottom line

The best tool to value my small business runs FCFF, FCFE, and EV/EBITDA on your actual financials, blends them for your specific decision context, recalculates as your books evolve, and lets you test strategic scenarios in plain English. XIT Matters delivers that engine free during beta in about ten minutes — no appraisal wait, no single-multiple guess, no stale report gathering dust. Know your number. Update it quarterly. Make every major decision against a scoreboard that actually reflects what you have built.