Why solopreneurs need a dedicated exit planning tool — not a generic calculator

If you are searching for the best exit planning tool for solopreneurs, you already sense that your business is not a miniature corporation. You are the product, the salesperson, the quality control, and often the only person who knows where the passwords live. That reality changes every assumption a buyer makes about risk, continuity, and price. Generic valuation widgets ignore it entirely. Formal appraisals capture it in a footnote you read six weeks later. What you need is a living model that treats owner dependency as a first-class input — something you can move on a slider and watch the walk-away number respond in real time.

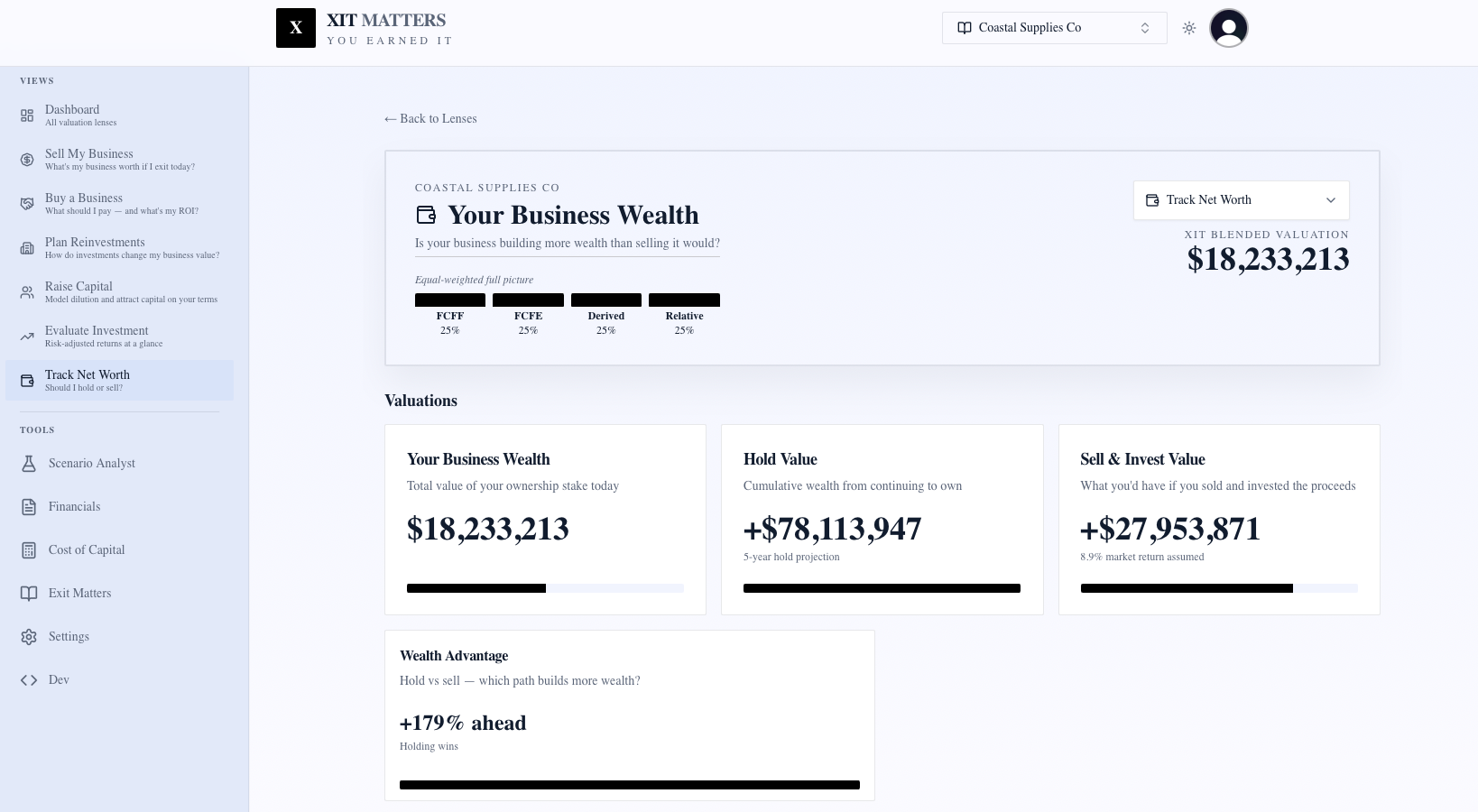

Exit planning for a one-person operation is less about picking a retirement date and more about answering three questions with numbers attached: What is my business worth to a financial buyer today? What would it be worth if I spent eighteen months productizing my delivery and shifting clients to retainers? And what do I personally need to net after taxes and debt to fund the next chapter? The best exit planning tool for solopreneurs connects those questions to the same three institutional methods professional valuators use — Free Cash Flow to the Firm, Free Cash Flow to Equity, and EV/EBITDA — then blends them with seller-weighted priorities so the headline answer matches the negotiation you are actually preparing for.

The solopreneur discount nobody talks about until diligence

Buyers do not buy your calendar. They buy cash flows that survive without you. For solopreneurs, that gap is the single largest valuation drag — often a full turn on the EBITDA multiple or a 15 to 25 percent haircut on intrinsic value through a higher discount rate.

The discount shows up in four predictable places. First, customer concentration: when your top three clients represent more than 40 percent of revenue, a buyer models the loss of any one of them as catastrophic. Second, delivery dependency: if you personally perform more than half of billable work, the buyer must budget for a replacement at market salary plus a transition period where quality may slip. Third, revenue mix: project-based work without recurring contracts signals lumpy cash flows that compress multiples. Fourth, undocumented processes: if the playbook lives in your head, the buyer prices in six to twelve months of chaos during handoff.

Exit Matters Chapter 12 frames timing as a function of readiness, not calendar age. For solopreneurs, readiness means making the business look like an asset instead of a job. The best exit planning tool quantifies each readiness gap so you know which lever returns the most dollars per hour of work you invest before going to market.

Three institutional lenses — adapted for a one-person shop

Professional valuators never rely on a single number. They triangulate. For solopreneurs, each lens exposes a different facet of the same underlying question: is this a business or a well-paid job?

FCFF — what the operations are worth unlevered

Free Cash Flow to the Firm projects the cash your business generates after taxes and reinvestment, discounts it at your weighted average cost of capital, and applies an illiquidity discount because private solopreneur businesses cannot be sold on an exchange. For service-based solopreneurs, the critical normalization step is replacing owner compensation with a market-rate salary for whoever would deliver the work post-acquisition. Skip that step and FCFF looks artificially high — then collapses in diligence when the buyer adds back a $120K replacement cost you never modeled.

FCFE — what lands in your pocket after obligations

Free Cash Flow to Equity strips out debt service and net borrowing to show what equity holders actually receive. Most solopreneurs carry minimal traditional debt but may have equipment loans, SBA balances, or merchant cash advances tied to revenue. FCFE keeps the boundary sharp between enterprise value and your personal walk-away. When you are modeling an exit where you carry a note for the buyer, FCFE is the lens that tells you whether the deal structure actually funds your next chapter.

EV/EBITDA — the language buyers speak

Market multiples anchor to what comparable one-person and micro-businesses have transacted at in your category. For professional services solopreneurs, typical SMB multiples sit between 2.5× and 5.0× normalized EBITDA depending on recurring revenue, client diversification, and documented SOPs. The multiple is never a fact — it is a band. The best tool shows low, median, and premium and maps each to the qualitative drivers you control: retainer mix, customer concentration, and owner hours in delivery.

Chapter 7 of Exit Matters explains how the Blended View weights these three lenses based on your decision context. For exit planning, the seller persona over-weights EV/EBITDA because that is what a financial buyer will anchor to — while still showing FCFF and FCFE so you understand the full range.

What the best exit planning tool for solopreneurs must do that spreadsheets cannot

Spreadsheets break the moment you ask a second question. Exit planning is inherently iterative — you need to test dozens of scenarios without rebuilding formulas each time.

Owner-dependency modeling. Move a slider from "I deliver 80% of billable work" to "I deliver 20%" and watch the EV/EBITDA multiple expand. That single interaction tells you whether hiring an associate or productizing a service offering is worth more than another year of grinding solo.

Recurring revenue conversion. Shift 30 percent of project revenue to monthly retainers and observe FCFF stability improve alongside multiple expansion. Buyers pay for predictability; the tool should make that trade visible in dollars.

Tax-aware walk-away. Exit is not enterprise value — it is what you keep after capital gains, debt payoff, and transaction costs. FCFE plus a seller-persona blend gets you closer to that personal number than any revenue multiple ever will.

Living, not static. Your books change monthly. A plan built on January numbers is stale by April. The right tool recalculates the moment inputs update so your eighteen-month roadmap reflects reality.

Plain-English scenario engine. Ask "What if I raised my hourly rate 15% and lost two clients?" and see the dollar impact across all three methods without touching a spreadsheet. The AI Scenario Analyst in XIT Matters translates questions like these into precise lever moves.

How XIT Matters maps to the solopreneur exit planning workflow

XIT Matters was built from the Exit Matters methodology with the solopreneur's constraints in mind — limited time, commingled books, and a business that genuinely depends on one person.

The onboarding flow accepts QuickBooks or Xero data or manual entry in about ten minutes. The seller persona automatically weights the Blended View toward EV/EBITDA while surfacing FCFF and FCFE tiles for context. Owner-dependency, customer concentration, and recurring-revenue mix appear as adjustable inputs tied directly to multiple bands.

The Cost of Capital Simulator exposes the four levers that move FCFF — credit spread, beta, debt paydown, and effective tax rate — with industry benchmarks for solo professional services. The Real-Time Slider Modeling lets you drag growth, pricing, and working-capital assumptions and watch every method recalculate instantly.

For exit planning specifically, the Tactical and Strategic Scenarios panel supports the eighteen-month playbook: model hiring a junior associate, converting clients to retainers, documenting SOPs, and reducing personal delivery hours — then compare today's blended valuation to the projected valuation at month eighteen. That delta is your ROI on exit prep.

Six Persona Views let you see the same business through seller, buyer, and investor lenses. Before you hire an M&A advisor, switch to the buyer persona and understand exactly how a financial acquirer will underwrite your key-person risk — then fix the gaps the model exposes.

Building your eighteen-month solopreneur exit roadmap

Start with a baseline valuation using current books — imperfect is fine; the tool flags what to clean up. Identify the two largest discount drivers the model surfaces. For most solopreneurs, those are owner delivery hours and customer concentration.

Month one through six: document every repeatable process, shift at least three clients to retainer or subscription billing, and hire fractional help for delivery or admin so your personal billable hours drop below 50 percent. Re-run the valuation quarterly and track multiple movement.

Month seven through twelve: diversify the client base so no single customer exceeds 15 percent of revenue, build a simple CRM pipeline that does not depend on your memory, and normalize owner compensation in the books so diligence does not surface surprises. Model a "ready to market" scenario in the tool and compare to baseline.

Month thirteen through eighteen: engage an M&A advisor or business broker if you want representation, or begin direct outreach to strategic acquirers in your niche. Walk in with the three-method range printed and one scenario showing your post-improvement valuation. Buyers respect sellers who understand their own math.

Throughout the window, use the AI Scenario Analyst to pressure-test deal structures — asset sale versus stock sale, earn-out percentages, seller financing terms — and see how each affects FCFE and your personal walk-away.

Common solopreneur exit planning mistakes to avoid

Waiting until burnout forces a sale compresses multiples and limits negotiation leverage. Buyers smell distress and structure earn-outs that keep you working years longer than you planned.

Using revenue multiples alone ignores the normalization adjustments that determine EBITDA — and EBITDA is what buyers actually multiply. A solopreneur showing $500K revenue with $350K in owner add-backs does not trade at the same multiple as a $500K business with $80K in true EBITDA.

Ignoring working capital surprises kills deals at the eleventh hour. Buyers expect a normalized net working capital peg; if your receivables ballooned or you deferred vendor payments, the purchase price adjusts down. Model working-capital days in the tool before you share any number.

Skipping the personal number. Enterprise value means nothing if FCFE after debt, taxes, and transaction costs does not fund your next chapter. Exit planning that stops at EV/EBITDA without a seller-weighted blend is incomplete for solopreneurs.

How solopreneurs compare exit planning tools side by side

When you evaluate the best exit planning tool for solopreneurs against alternatives, score each option on five criteria: does it run all three institutional methods, does it model owner dependency as an input, does it recalculate as your books change, does it support seller-weighted blending, and can you test scenarios in plain English without rebuilding spreadsheets? Spreadsheets fail the living-recalculation test. Generic calculators fail the three-method test. One-time appraisals fail the scenario and timeline tests. XIT Matters passes all five — which is why solopreneurs use it as the financial backbone of an eighteen-month exit plan rather than a one-time number pinned to a wall.

The bottom line for solopreneurs planning an exit

The best exit planning tool for solopreneurs is not a calendar reminder or a generic multiplier. It is a living valuation engine that treats owner dependency, recurring revenue, and customer concentration as adjustable inputs — runs the same FCFF, FCFE, and EV/EBITDA stack institutional buyers expect — and lets you test eighteen months of improvements before you ever pick up the phone. XIT Matters delivers that stack free during beta, recalculates as your books evolve, and translates plain-English what-ifs into exact dollar impacts across every method. Start with today's number, fix the two biggest discounts the model surfaces, and walk into your exit conversation knowing the math behind your ask.