How to get an accurate business valuation fast (free) — the 80/20 path

If you are searching how to get an accurate business valuation fast (free), you are rejecting two bad options: wait six weeks and pay $5,000–$25,000 for a formal report you cannot act on until it arrives, or trust a revenue-multiple widget that ignores your capital structure, working capital, and industry band position. The third path runs the same three institutional methods professional buyers underwrite — Free Cash Flow to the Firm, Free Cash Flow to Equity, and EV/EBITDA — blends them for your decision context, and delivers a defensible range in about ten minutes at zero cost during the XIT Matters public beta.

Exit Matters Chapter 3 states the 80/20 rule plainly: capture directional accuracy you can act on today rather than perfect precision delivered months from now. Chapter 7 introduces the Blended View — three lenses weighted toward the decision in front of you. Speed without method is a guess. Method without speed is a backlog. Accurate and fast requires both.

Step 1 — Gather and normalize your financials (fifteen minutes or less)

Pull two years of P&L, current balance sheet, and trailing cash flow. Before any valuation engine runs, normalize earnings:

Remove one-time legal, repair, and marketing spikes. Adjust owner compensation to market rate — neither inflated perks nor artificially low salary. Review working capital: days sales outstanding, inventory turns, vendor terms. Buyers rebuild EBITDA in diligence; starting clean prevents surprise downward adjustments.

Connect QuickBooks or Xero compatible import or enter summaries manually. Imperfect books are acceptable for a first pass — refine as accounting improves and the living valuation updates automatically.

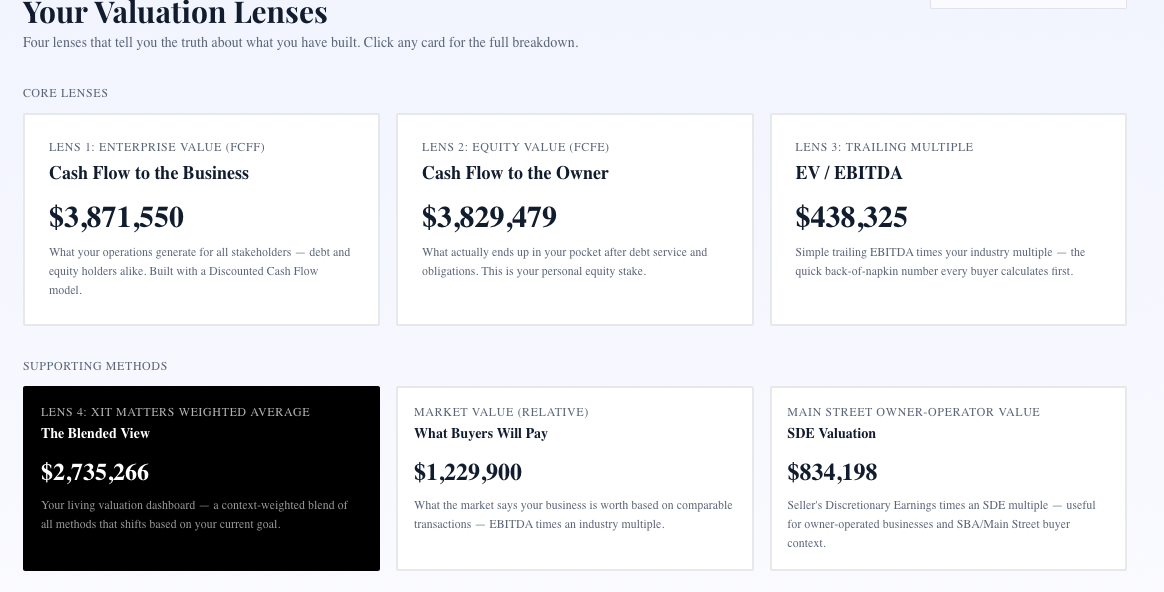

Step 2 — Run FCFF, FCFE, and EV/EBITDA in parallel

FCFF (enterprise/intrinsic). Project unlevered cash the operations generate, discount at weighted average cost of capital, apply illiquidity discount appropriate for private SMB equity. Output: what the whole business is worth to all capital providers.

FCFE (equity/walk-away). Same cash flow machinery after debt service and net borrowing adjustments, discounted at cost of equity. Output: what your shares are worth — critical for personal wealth, dilution, and sale proceeds.

EV/EBITDA (market anchor). Apply industry multiple band — low, median, premium — to normalized EBITDA with adjustments for customer concentration, recurring revenue, owner dependency, and growth visibility.

No single lens tells the whole truth. Triangulation produces the range you can defend.

Step 3 — Apply persona-aware blending

Switch blending weights to match your decision:

Day-to-day operations: More weight on FCFF and FCFE — cash flow stability drives reinvestment choices.

Preparing to sell: More weight on EV/EBITDA — buyers anchor on market comps.

Raising capital: More weight on FCFE — dilution math requires equity value clarity.

The same financials produce different blended headlines under different personas — both valid, both useful.

Step 4 — Stress-test with one scenario

Accuracy improves when you test sensitivity. Ask one plain-English question: price increase, strategic hire, debt paydown, or customer diversification. Confirm dollar deltas appear across all three methods and the blended headline. If only one method moves, the engine is incomplete.

XIT Matters AI Scenario Analyst and Real-Time Slider Modeling handle this in seconds after baseline setup.

Step 5 — Document assumptions and schedule a refresh

Save your baseline, note normalized EBITDA, multiple band position, and persona weighting used. Re-run monthly or quarterly as books improve — accuracy compounds when the valuation stays live, not frozen in a PDF.

Why generic calculators fail the accuracy test

Single revenue or EBITDA multiples collapse distinct businesses into one number. They ignore WACC sensitivity, net debt, working-capital quality, and industry premium drivers. They deliver the same answer whether you are operating or selling. They cannot show which operational fix moves value most.

Institutional triangulation forces every assumption into the open — growth rate, margin sustainability, capital intensity, market band position. That is how to get an accurate business valuation fast (free) without pretending a widget equals an appraisal.

Accuracy expectations — what "fast and free" can and cannot promise

With clean normalized financials, three-method blended answers typically land within 10–20 percent of later CPA-issued ranges. Messy books, unusual capital structure, or thin transaction comps widen variance — the platform flags low-confidence inputs so you know where to dig deeper.

Fast and free delivers directional accuracy for decisions — hire, price, borrow, prepare for sale. It does not deliver signed fairness opinions for litigation, divorce, or IRS filings. Budget formal work when binding stakes require it.

A worked example — $2.8M revenue professional services firm

Normalized EBITDA $520K, moderate owner dependency, top customer 18 percent of revenue, modest equipment debt.

Generic calculator: 4× EBITDA = $2.08M — done.

Three-method stack: FCFF intrinsic $2.4M–$2.7M after WACC and illiquidity discount. FCFE equity $2.1M–$2.4M after debt service. EV/EBITDA at median 3.8× = $1.98M; at premium 5.0× = $2.6M. Blended owner persona $2.2M–$2.5M; seller persona $2.0M–$2.3M with more market weight.

The owner now has a range, sees FCFF–market gap as operational uplift opportunity, and knows fixing owner dependency expands the band — not just hoping for a better offer.

How XIT Matters delivers accurate valuation in ten minutes

Blended Valuation Engine runs FCFF, FCFE, and EV/EBITDA simultaneously.

Six Persona Views shift blending weights instantly.

Cost of Capital Simulator exposes WACC and cost of equity drivers — not fixed 12 percent guesses.

EV/EBITDA Market Comps with industry bands and premium/discount driver lists.

Real-Time Slider Modeling and AI Scenario Analyst for sensitivity and compound questions.

QuickBooks and Xero compatible import or manual entry — free during beta, no credit card.

Approved trust claims: Built from Exit Matters, methodology used by PE firms, ten minutes to your first valuation.

When to escalate from fast free to formal appraisal

Engage CPA-led Quality of Earnings or formal appraisal for signed LOI diligence, partner buyouts with adversarial parties, litigation, divorce, and IRS estate or gift filings. Use the fast free valuation to arrive prepared — range in hand, fix list prioritized, scenarios rehearsed — so formal work starts from knowledge, not blind trust.

The bottom line

How to get an accurate business valuation fast (free) in 2026: normalize earnings, run FCFF + FCFE + EV/EBITDA, blend for your persona, stress-test one scenario, refresh monthly. XIT Matters automates that workflow in ten minutes at zero cost during beta. Stop waiting for perfect books or perfect appraisers. Start with a defensible range you can act on today.

Normalization checklist — the fastest path to accuracy

Before you trust any fast valuation, walk this checklist: owner compensation at market rate, personal expenses removed from P&L, one-time legal and repair costs excluded, inventory and receivables aged appropriately, related-party rent at market terms. Each item takes minutes to fix in your worksheet but prevents hours of credibility loss in a buyer or lender conversation. Accuracy in how to get an accurate business valuation fast (free) comes from normalized inputs, not from a fancier algorithm hiding bad data.

Comparing your fast valuation to broker verbal estimates

Brokers sometimes quote ranges verbally without methodology — often anchored to recent comps that may not match your earnings quality. Run your three-method blend first, then compare broker quotes to your FCFF–FCFE–EV/EBITDA convergence zone. When broker high ends exceed your market lens materially, ask which premium drivers they believe you have earned. When broker lows sit below your FCFE floor, you know where to push back. Fast free valuation gives you independent methodology before you depend on someone else's incentive structure.

Industry band placement — moving from discount to median

Every industry ships a low, median, and high multiple band in XIT Matters. Identify which discount drivers still apply to your business — owner dependency, customer concentration, volatile earnings, messy financials — and model fixing each. The fastest accuracy improvement is often operational: document SOPs, diversify customers, normalize owner pay, clean working capital. Each fix moves band position; remeasure monthly. How to get an accurate business valuation fast (free) becomes a management habit, not a one-time calculator visit.

Speed versus precision — when to stop iterating

Exit Matters Chapter 3 advises stopping when additional precision changes the blended view less than 10–15 percent. For fast free valuation, that means do not chase perfect lease capitalization on a $40K line item if your blended range already supports the hire-or-sell decision. Iterate until the range is tight enough for the decision at hand — banker meeting, partner buyout talk, internal capital allocation — then execute. Perfection is the enemy of the ten-minute valuation that actually gets used.

Pairing fast valuation with advisor conversations

Bring your three-method range to your CPA, banker, or M&A advisor as a starting point — not as gospel. Advisors add normalization you missed, comps you did not see, and structure you have not modeled. The fast free pass makes their time more efficient because you speak institutional language from the first minute. That is how owners compress weeks of back-and-forth into focused sessions that move decisions forward instead of restarting from a revenue multiple guess.

Red flags that your fast valuation is wrong

If FCFF and EV/EBITDA diverge by more than 40 percent with no clear story, check normalization and multiple band placement — one input is likely wrong. If FCFE exceeds FCFF, debt modeling may be inverted. If every method matches a generic calculator exactly, you are probably running a single multiple dressed as three numbers. If WACC never moves when you change customer concentration or growth assumptions, the engine is using static defaults. How to get an accurate business valuation fast (free) still requires sanity checks; speed is worthless if the range fails basic triangulation logic.

Document your first run — template for monthly refresh

Record date, normalized EBITDA, net debt, industry band position (discount, median, premium), persona used, and blended range. Next month, change only what changed in the business — one fix, one new customer, one debt payment — and remeasure delta. Owners who log twelve consecutive monthly runs report tighter ranges and faster advisor meetings because the history tells a story spreadsheets scattered across email cannot. The ten-minute habit compounds into institutional fluency: you stop asking whether the number is vaguely right and start managing toward a range you can explain line by line.

Final reminder — fast, free, and honest about limits

How to get an accurate business valuation fast (free) works when you treat output as a living range tied to normalized financials, not a certificate on the wall. XIT Matters delivers FCFF, FCFE, EV/EBITDA, persona blending, and scenario sensitivity in one sitting — free during beta. Use it for speed and direction; use formal appraisal when the law or the deal requires a signature. That division is the 80/20 path Exit Matters describes, and it is how busy owners finally know what they are worth without waiting for permission from a $25,000 engagement letter.