What is my consulting business worth? Start with the 2026 multiple band, not a guess

If you are asking what is my consulting business worth, the honest answer is a range — not a single number from a broker's rule of thumb. Consulting firms in the typical SMB band ($500K to $15M revenue) trade on trailing twelve-month EBITDA multiplied by industry-specific comps: 2.5× at the low end, 3.8× at the median, and 5.5× at the high end before net debt adjustment. Where you sit on that band depends on retainer mix, founder dependency, client concentration, and whether your methodology survives without you in the room. A revenue multiple pulled from a blog post ignores those drivers and routinely misprices boutique firms by hundreds of thousands of dollars.

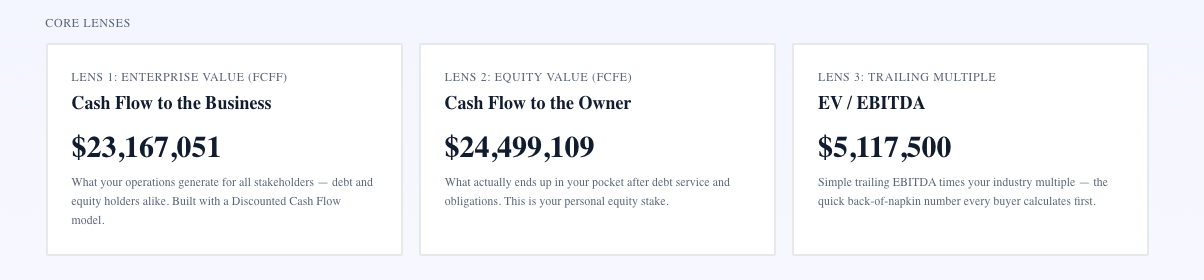

Exit Matters Chapter 6 frames what buyers pay for in professional services — predictable cash flows, transferable client relationships, and delivery that does not collapse when the founder leaves. Chapter 4 converts those cash flows into present value through FCFF. Chapter 7 blends FCFF, FCFE, and EV/EBITDA into one decision compass. What is my consulting business worth becomes a question you answer with three lenses, not one.

The consulting multiple band explained — low, median, and premium

Low (2.5× EBITDA) fits hours-billed staff augmentation, project revenue without renewals, and firms where the founder is the brand and primary billable resource. Buyers treat these as job shops with key-person risk.

Median (3.8× EBITDA) fits mixed retainer and project revenue, some bench depth beyond the founder, and multi-year relationships on a meaningful share of the book. Financials are clean; owner compensation is normalized.

High (5.5× EBITDA) fits boutique strategy and management-consulting firms with repeatable IP, renewals that survive leadership transition, and delivery teams operating independently of the founder. Pure staff-aug shops rarely reach this tier.

Premium drivers: repeatable IP or methodology, multi-year client relationships, bench depth beyond founder. Discount drivers: hours-billed model, founder-led delivery, project mix without renewals. Boutique strategy firms can clear 5×; staff-aug compresses to 2.5×–3.0×.

Normalize earnings before any method runs

Consulting owners often mix personal and business expenses, underpay or overpay themselves relative to market, and book one-time projects that distort year-over-year comparisons. Before FCFF, FCFE, or EV/EBITDA can be trusted:

Replace owner compensation with market-rate cost for the roles you perform — rainmaker, delivery lead, practice manager.

Remove non-recurring project revenue and associated costs that will not repeat.

Adjust for clients who paused or churned — buyers underwrite forward revenue, not peak year nostalgia.

Review DSO on large engagements; slow-paying enterprise clients affect working-capital quality in FCFF.

Normalized EBITDA is the input every method shares. Skip normalization and you argue from a number diligence will rebuild downward.

Run FCFF, FCFE, and EV/EBITDA on your consulting numbers

FCFF measures cash the practice generates for all capital providers before financing. For consulting, reinvestment is usually people and systems — not heavy capex. Working capital swings on receivables matter more than equipment.

FCFE is what remains for equity holders after debt service and reinvestment. Partner buyouts and personal wealth planning hinge on this lens. Enterprise value without FCFE misleads owners who confuse headline price with walk-away cash.

EV/EBITDA applies your position on the 2.5×–5.5× band to normalized EBITDA. Move the multiple slider using premium and discount drivers — retainer mix, concentration, owner dependency — and see market anchor shift in real time.

The Blended View weights the three lenses toward your decision. Active owners tracking wealth may weight FCFF and FCFE; sellers prepping a transaction weight EV/EBITDA while keeping cash-flow tiles visible.

Drivers that move consulting firms up the band

Retainer and renewal mix. Convert project clients to annual agreements where scope allows. Model 20-point shifts in recurring percentage and measure multiple expansion.

Methodology and IP. Document frameworks, templates, and delivery playbooks buyers can transfer. Productized assessments and subscription advisory offerings signal durability.

Bench depth. Hire or promote senior managers who own client relationships. Reduce your billable hours while maintaining revenue — the classic key-person fix.

Customer diversification. No single client above 15–20 percent of revenue. Concentration above 25 percent compresses multiples predictably.

Clean financials. Separate personal expenses, consistent chart of accounts, auditable time tracking. Quality of earnings starts with books buyers can trust.

Each driver maps to sliders in XIT Matters — fix the two largest gaps before you engage a broker or answer a partner buyout offer.

What is my consulting business worth to different counterparties?

To you as owner-operator. FCFF and FCFE under owner persona weighting — wealth tracking and reinvestment decisions.

To a strategic acquirer. EV/EBITDA with synergy uplift possible if your client base or methodology fills a gap — your XIT range is often the floor, not the ceiling.

To a financial buyer. EV/EBITDA anchored to the band with key-person and concentration discounts applied — seller persona rehearsal shows their likely opening bid.

To a departing partner. FCFE under agreed buyout structure — model note terms, earn-out, and normalized compensation before signatures.

Same business, different lens — the Blended View prevents arguing from the wrong number in the wrong conversation.

Common mistakes when estimating consulting firm value

Using last year's peak project revenue as run-rate. Buyers forward-underwrite; lumpy years need normalization.

Ignoring owner dependency because "clients love me." Goodwill is not transferable goodwill until delivery survives your exit.

Applying agency or SaaS multiples to consulting firms. Industry bands differ; wrong benchmark, wrong range.

Stopping at enterprise value in partner talks. FCFE after structure determines fairness.

Waiting for perfect books. Start with directional range; refine quarterly as accounting improves.

Building a twelve-month value improvement plan for consulting firms

Month one: run baseline and identify the two largest discount drivers — usually founder dependency and client concentration. Month two through four: model retainer conversion on your top five project clients; set measurable recurring-revenue targets. Month five through seven: hire or promote senior delivery leaders; track owner billable hours declining while revenue holds. Month eight through ten: document methodology — frameworks, templates, engagement playbooks — so buyers see transferable IP. Month eleven through twelve: re-run seller-weighted blend and compare to month-one baseline; the delta is your value-creation scorecard.

Consulting owners who follow this cadence often move one full multiple turn over eighteen months — on $800K EBITDA, that is $800K of enterprise value from operational fixes you control, independent of market sentiment. XIT Matters quantifies each leg of the plan so you prioritize hires and sales process changes by blended ROI, not instinct.

Partner buyouts and succession — FCFE is the number that matters

When a partner exits, the conversation starts with enterprise value and ends with structure. A $4M EV headline with 30 percent seller note at below-market interest and three-year earn-out tied to metrics the departing partner no longer controls may produce FCFE well below a $3.5M all-cash alternative. Model both before term sheets circulate.

Normalized compensation matters in partner disputes — if one partner has been underpaid for delivery and another overpaid for rainmaking, EBITDA normalization affects everyone’s share. Run scenarios with market-rate owner compensation for each role before lawyers draft buyout language.

Consulting versus adjacent professional services — use the right band

Do not benchmark against digital agencies if you are a pure consulting shop — agency bands center higher when productized retainers exceed 60 percent. Do not benchmark against SaaS if you have no recurring software revenue. The consulting record in industry multiples — 2.5× low, 3.8× median, 5.5× high, typical revenue $500K–$15M — is the correct anchor for boutique advisory, strategy, and management consulting firms.

When you still need a formal appraisal

Binding partner buyouts under dispute, divorce, estate planning, litigation, and lender-required opinions need CPA-signed deliverables. Self-served three-method valuation accelerates preparation — you know your range and lever sensitivity — but does not replace signed opinions when stakes are adversarial. Budget formal work when the event is binding; use XIT Matters for everything leading up to it.

Practice size — where consulting firms typically land on the band

A solo practitioner with $600K revenue and $250K normalized EBITDA after owner add-back often compresses toward 2.5×–3.0× when the founder delivers every engagement. A ten-person boutique with $4M revenue, 55 percent retainer mix, and two partners who do not lead delivery may approach 3.8×–4.5× when financials are clean and concentration is manageable. A $12M management-consulting firm with proprietary methodology, enterprise clients, and a bench of engagement managers can reach the 5.0×–5.5× tier — but only when diligence confirms those claims with contracts and utilization data.

What is my consulting business worth depends on which of those profiles matches your reality, not which headline multiple you hope for. Run the three methods on normalized numbers and read your band position honestly before you enter partner talks or buyer outreach. If your profile sits between tiers, model both — conservative and stretch — and plan operational moves toward the higher tier over the next four quarters.

Due diligence checklist for consulting firm sellers

Prepare these before you share a range with any counterparty: three-year P&L with EBITDA normalization memo, client list with revenue concentration, retainer contract schedule, org chart with billable rates and utilization, documented methodology assets, and a narrative explaining how delivery continues if you reduce hours 50 percent. Buyers discount what they cannot verify. XIT Matters scenario outputs supplement the narrative with dollar impact — hire scenario, retainer conversion scenario, concentration reduction scenario — so your asking range is backed by operational math, not optimism.

Consulting founders who treat this checklist as a twelve-month operating plan — not a last-minute data room scramble — routinely move one band tier before they engage a broker. What is my consulting business worth becomes a scoreboard you update quarterly instead of a question you panic-answer when a buyer calls. Pair each checklist item with a scenario in XIT Matters so every operational fix shows up as dollars on the blended headline, not just a bullet on a slide deck. Buyers and partners respect founders who arrive with ranges, drivers, and a plan — what is my consulting business worth stops being abstract when every initiative ties to measurable multiple movement. Start with your baseline this week; refine as books improve and your band position becomes clearer each quarter.

The bottom line — what is my consulting business worth in 2026

What is my consulting business worth? For most SMB consulting firms in 2026, the defensible answer sits in the 2.5×–5.5× normalized EBITDA band — exact position driven by retainer mix, founder dependency, client concentration, and bench depth — validated by FCFF and FCFE convergence. XIT Matters runs all three methods on your financials in ten minutes, surfaces consulting premium and discount drivers beside the slider, and models operational fixes in dollars on the blended headline. Free during beta. Know your range before a buyer, partner, or advisor names theirs.